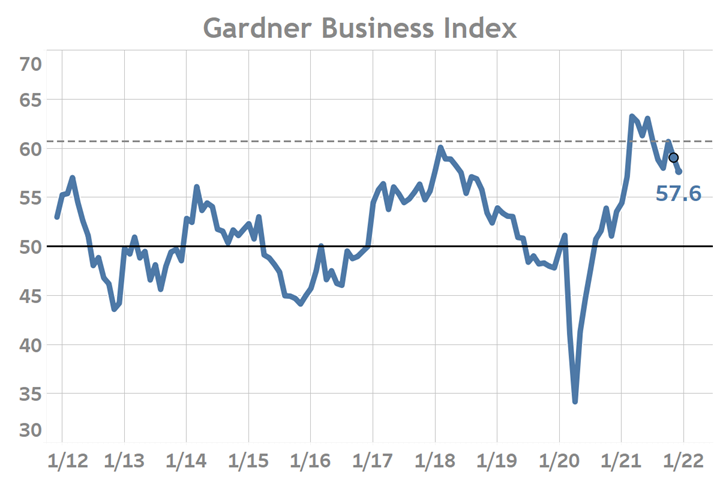

Gardner Business Index - December 2021: 57.6

GBI Ends 2021 Slightly Better Than Where the Year Started

.jpg;width=70;height=70;mode=crop)

Share

The Gardner Business Index (GBI) closed out 2021 with a December reading of 57.6, three-points higher than where it started the beginning of the year and almost 6-points below its March 2021 peak. December’s readings extended the business activity trends of the second half of the year. Those trends included the slowing acceleration of supply chain activity, production, and new orders. December exports activity remained unchanged, extending the year’s string of generally tranquil results. Payroll activity for both the month and the second half of the year also decelerated, but to a relatively lesser degree when compared to production and new orders. This is not surprising given that historically payroll activity directionally follows that of new orders and production with a near two-quarter delay. Assuming this historic relationship holds true, payroll activity can be expected to further slow in the first half of 2022.

The Gardner Business Index (GBI) ended 2021 only modestly higher than where it started at the beginning of the year and well off its 1Q2021 peak.

December’s supply chain activity reading fell nearly 4-points and now stands approximately 7-points below its 2021 —as well as all-time— high reading in excess of 82-points. Declining readings which remain above a level of ‘50’ indicate that a rising proportion of manufacturers are reporting either no-change in month-to-month supply chain performance or even improving supply chain delivery timeliness. Should supply chain readings continue to move lower going into 2022 as supply chain performance improves one might expect production activity to increase as material procurement becomes less of a bottleneck. Greater production relative to sustained new orders activity could also drive lower backlog readings.

Should this assessment for 1H2022 prove true, the industry could see lower overall GBI readings as supplier delivery, backlog and employment readings fall while production increases. Yet these changes would point to an industry slowly headed towards a much healthier and sustainable position. Even if the latest trend in supplier delivery readings (roughly a 7-point decline per six-month period, or 14-points on an annualized basis), it would be mid-2023 before supply chain readings return to their long-run levels.

A Note About Gardner Intelligence and the GBI:

Gardner Intelligence does its utmost to provide regular and informative updates on the state of manufacturing especially given the challenges posed by COVID-19. Gardner cannot thank our survey participants enough for their insights and on-going support. We hope that you will continue to tell us how your businesses are faring. Only through your participation are we able to assess the current state of the industry and where it may be heading. We would encourage our followers and publication subscribers to regularly visit our website blog and connect with Gardner Intelligence on LinkedIn and see our YouTube Channel.