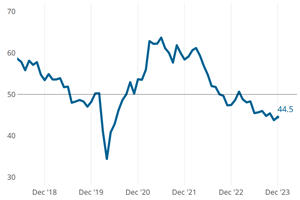

Metalworking activity continued to contract in what has become a rather characteristic GBI ‘dance.’

Steady contraction of production, new orders and backlog drove accelerated contraction in November.

October marks a full year of metalworking activity contracting, barring just one isolated month of reprieve in February.

Metalworking activity has contracted since October of 2022.

The degrees of accelerated contraction are relatively minor, contributing to a mostly stable index despite the number of components contracting.

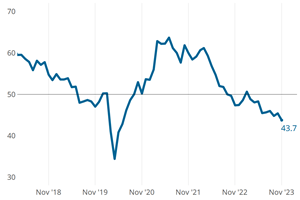

Metalworking activity hung together better in July, with all but one GBI component contracting.

Components that contracted include new orders, backlog and production, landing on low values last seen at the start of 2023.

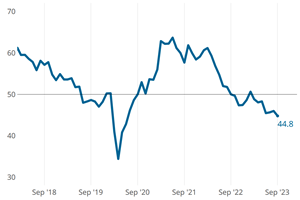

Four components contracted slightly more than in April, including production, new orders, exports and backlogs.

The GBI Metalworking Index in April looked a lot like March, contracting at a marginally greater degree.

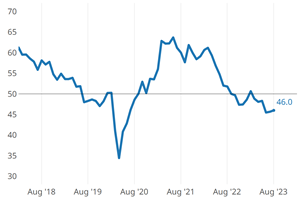

February’s call for cautious optimism was well placed…market dynamics in March put a damper on what had been metalworking activity’s modest re-entry to growth mode in February.

The GBI closed at 50.6 in February, calling for cautious optimism.

Most components held steady in January, but new orders and exports showed ever-so-slight slowing of contraction.