Beware of COVID's Misleading Impact on Diffusion Indices

COVID’s unique impact on the manufacturing economy and beyond means that the normal interpretation of diffusion indices around the world needs a re-think. The breakdown of supply chains has distorted the reading for supplier deliveries, causing the GBI and other indices like it to register inflated readings. The solution to this is to watch the index components independently with added attention given to new orders and production.

.jpg;width=70;height=70;mode=crop)

Share

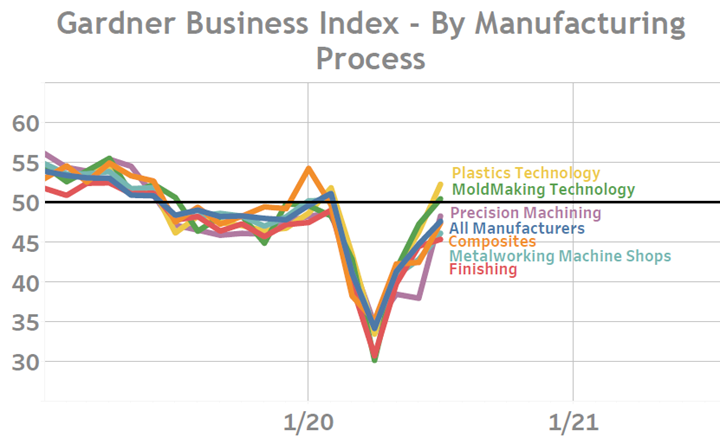

Gardner Intelligence collects business activity data across many different segments of the manufacturing sector. These segments align with Gardner’s print magazine publications including Modern Machine Shop (Metalworking), Production Machining (Precision Machining), Products Finishing (Finishing), MoldMaking Technology (Moldmaking/Molding), Plastics Technology (Plastics and Plastics Processing) and Composites World (Composites Fabrication). Each of these segments has its own business index thanks to Gardner’s broad and deep connections to over 200,000 U.S. manufacturers. The entirety of the survey responses collected monthly from all of these manufacturers are used to produce what is simply called the “Gardner Business Index” and published on our website: www.gardnerintelligence.com/blog.

For each of these manufacturing segments, Gardner Intelligence also calculates independent business activity indices. This enables our readers to see how their specific segment of the manufacturing industry is being affected by the many common factors that impact all of manufacturing as well as those unique economic factors that exclusively shape their business environment.

The wide-spread disruption of the world economy as a result of the spread of COVID-19 presents a unique opportunity to witness how a single shock to the economy has since resulted in an array of different business conditions within the greater manufacturing industry. While the initial shock of COVID-19 sent all of Gardner’s segment indices to all-time lows during the second quarter of 2020, how each has fared since reaching those lows has varied considerably.

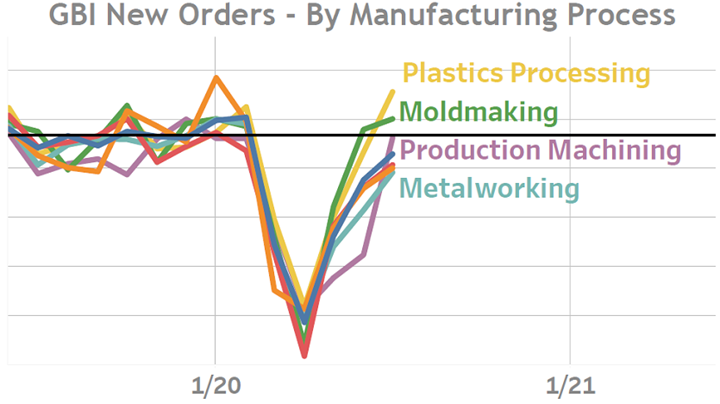

New Orders:

New orders activity is arguably the most important component of the business index. Changes in new orders directly affect production and backlog. It also has a delayed importance to supplier delivery and employment activity. For these reasons, it is considered a bellwether of the overall index. Across Gardner’s manufacturing indices, the path of new orders since April has served as a clear example of the uniqueness within each industry segment. Plastics Processing and Moldmaking have both seen new orders not only stabilize but also begin to rebound. The Finishing and Composites manufacturing segments have seen new orders continue to contract but at ever slowing rates. Lastly, Production Machining experienced a prolonged period of strongly contracting activity only to quickly transition to a near no-change condition by July.

Supplier Deliveries:

Dissimilar to the other components of the Index, the supplier deliveries section of the survey asks if supplier deliveries are ‘slower’, ‘the same’ or ‘faster’ compared to the prior month. During an economic expansion, demand from manufacturers for the upstream goods they need to make their own products can be very high. If those upstream suppliers cannot keep up with this heightened demand, the result will be a growing backlog of orders manifested through lengthened delivery times. Conversely, during an economic lull, manufacturers reduce their purchases of input goods allowing suppliers to deliver products quickly and without delay. To align supplier delivery activity with the manufacturing business cycle, slowing deliveries are calculated such that they raise the supplier delivery reading and lower it when deliveries are faster.

Unfortunately, 2020 has proven to be a year unlike any other. As government leaders from around the world have worked tirelessly to slow the spread of COVID-19, their efforts have had the unfortunate consequence of significantly disrupting domestic as well as global supply chains. It is because of this disruption, as opposed to strong demand for upstream products overall, that the supplier deliveries reading has moved higher while the economy has contracted.

The heightened readings of supplier delivery activity are therefore improperly elevating the “total” index reading. This is because the total index is calculated as the simple average of the index’s components (new orders, production, supplier deliveries, backlogs, exports and employment). As of the July data release, recent expansionary total index readings (readings above 50) were only possible because of elevated supplier delivery readings; without the inclusion of these readings, the total index would still indicate that manufacturing is in a slowing contraction. In conclusion, it is important for business leaders in manufacturing and beyond to monitor new orders and production readings with greater importance when examining any diffusion index which includes supplier deliveries as part of its total index calculation. This includes not only the Gardner Business Index but commonly referenced diffusion indices including the Institute for Supply Management’s Purchasing Managers Index (PMI).