Gardner Business Index - April 2020

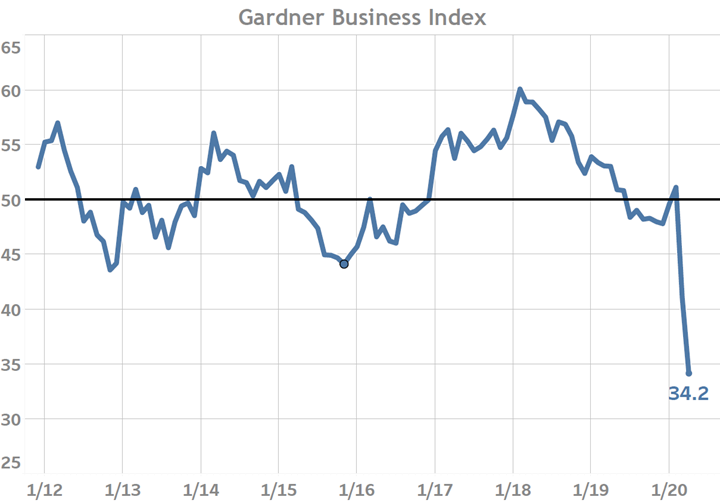

April’s reading of 34.2 signaled that overall business activity conditions continued to slow further after falling sharply in March.

Share

April’s reading of 34.2 signaled that overall business activity conditions continued to slow further after falling sharply in March. As expected, April’s data also indicated that the disruption to supply chains reported last month also further worsened. For a second month, new orders, production and exports activity led the Index lower. These components are considered leading indicators of the Index due to their frequent influence on backlogs and employment readings in later months.

The Index fell for a second consecutive month in April as COVID-19 continues to severely disrupt the manufacturing sector.

April’s activity contraction was widespread across the manufacturing sector. Manufacturers of all sizes and serving all end-markets reported further slowing business activity. The spread in the average index reading between firms under 20-employees and those over 250-employees over the last two-months was less than 1-point. During typical downturns large firms have more options available to them to cope with the pain of a downturn; however, the current situation has left little -if any- room for firms of any size to maneuver to relatively greater safety.

As reported last month, it is highly unusual to experience a combination of slowing supplier deliveries and weakening orders. More typically supplier deliveries slow when demand for upstream goods is high and backlogs increase, forcing deliveries to slow as a result of bottlenecks in upstream production. It is for this reason that the index reading for supplier deliveries is designed to increase (register above 50) when deliveries are slowing. However, in the present situation, the elevated supplier delivery readings reflect the severity of the disruption to both global and domestic supply chains as opposed to elevated upstream orders and backlogs.

Among the 24 end-markets tracked by Gardner, 21 experienced a quickening contraction in business activity in April while three reported slowing decline. Among the end-markets Gardner tracks, the construction machinery market faired substantially worse than all others, reporting an April reading of 20.8. Excluding construction machinery, the average index reading of the remaining 23 end-markets was 36.0. Despite the overall slowing of business for the sector, Gardner continues to receive anecdotal stories from firms who have lost much of their regular business and yet have received an ‘atypical’ order in the form of a large-volume order to produce one or a few products related to the battle against COVID-19. While not all firms can expect to receive such windfalls, it is important for firms to look for opportunities wherever possible and to always consider diversification as an important part of their business’ strategy.

Gardner cannot thank our survey participants enough for their insights and support. In March and now also April we received well-above our average number of monthly survey responses. This higher response rate helps ensure the accuracy of our reporting back to you, our readers, on the latest business conditions in the manufacturing sector. Only through your participation will we be able to gauge when this difficult period will pass and when we will see a new dawn on the horizon.