Real 10-Yr Rate Grinding Slowly Higher

The Federal Reserve has stated it will not pursue negative interest rates. Therefore, the only way for the change to be more negative is for inflation to increase, which is why the Federal Reserve has stated a new policy of average inflation targeting.

.JPG;width=70;height=70;mode=crop)

Share

In September, the nominal 10-year Treasury rate was 0.68%, which was the third lowest rate ever and just above the previous two months. Also, it was the seventh month in a row and the seventh month ever that the monthly average was below 1%. So, the nominal 10-year Treasury rate was at or hovered near its all-time lows for seven straight months.

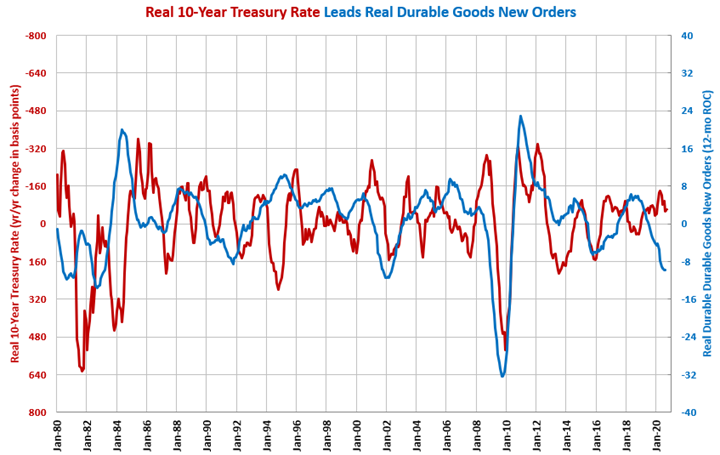

The real 10-year Treasury rate, which is the nominal rate minus the rate of inflation, was -0.76%. This was the ninth consecutive month and 12th of the last 14 that the real rate was negative. However, the rate was grinding slowly higher since April.

In September, the year-over-year change in the real rate was -60 basis points. The change was negative for the 21st month in a row. The change was near its highest level since January. Since April, the trend in the year-over-year change in the real 10-year Treasury was less negative. A less negative change in the real rate is less stimulating to the economy, which is not what the Federal Reserve wants.

However, the Federal Reserve has stated it will not pursue negative interest rates. Therefore, the only way for the change to be more negative is for inflation to increase, which is why the Federal Reserve has stated a new policy of average inflation targeting. This policy basically states that the Federal Reserve will allow inflation to run substantially higher than its target of 2% so that the long run average of inflation is 2%.

As much as the absolute level of interest rates, it is the relative change in interest rates that drives additional borrowing and spending. A falling change in the real 10-year Treasury rate tends to be a positive signal for durable goods manufacturing. Declining changes in the real 10-year Treasury rate tend to lead growth in durable goods new orders and capital equipment consumption by a relatively long period of time – historically, between 12 and 24 months. The longer-term declining change in the 10-year Treasury rate is a good leading indicator of growth in housing permits, construction spending and consumer durable-goods spending as well.