Real 10-Yr Rate Supporting Durable Goods Manufacturing

August 2020 was the eighth consecutive month and 11th of the last 13 that the real rate was negative.

.JPG;width=70;height=70;mode=crop)

Share

In August, the nominal 10-year Treasury rate was 0.65%, which was the second lowest rate ever. And, it was the sixth month in a row and the sixth month ever that the monthly average was below 1%. So, the nominal 10-year Treasury rate was at or hovered near its all-time lows for six straight months.

The real 10-year Treasury rate, which is the nominal rate minus the rate of inflation, was -0.81%. This was the eighth consecutive month and 11th of the last 13 that the real rate was negative. Inflation increased to its highest rate since March.

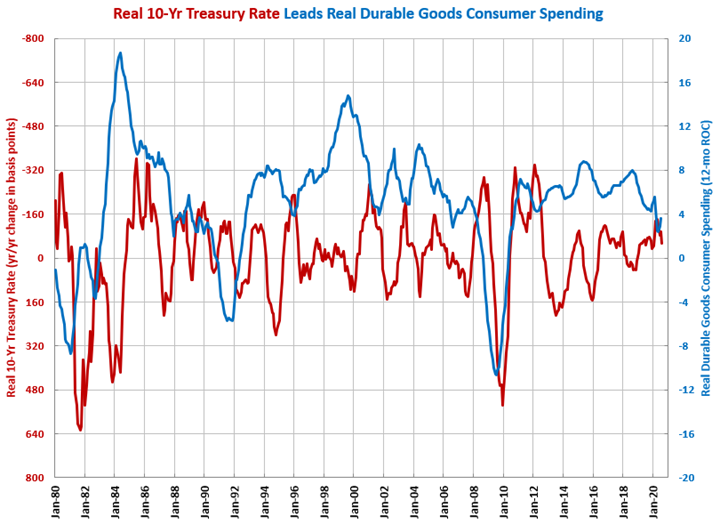

In August, the year-over-year change in the real rate was -54 basis points. The change was negative for the 20th month in a row. The change was at its highest level since January. In general, the trend in the year-over-year change in the real 10-year Treasury was moving down (more negative) in the last six years. In order for that trend to continue, the rate of inflation needs to accelerate since the Federal Reserve has stated it has no desire for nominal rates to go below zero.

As much as the absolute level of interest rates, it is the relative change in interest rates that drives additional borrowing and spending. A falling change in the real 10-year Treasury rate tends to be a positive signal for durable goods manufacturing. Declining changes in the real 10-year Treasury rate tend to lead growth in durable goods new orders and capital equipment consumption by a relatively long period of time – historically, between 12 and 24 months. The longer-term declining change in the 10-year Treasury rate is a good leading indicator of growth in housing permits, construction spending and consumer durable-goods spending as well.