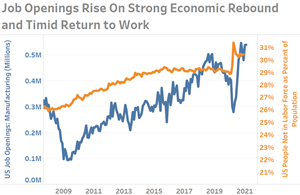

The number of unfilled manufacturing jobs during the initial months of 2021 has not been higher since the Great Recession. During most months since October 2020, the number of unfilled manufacturing jobs has exceeded 500,000. For reference, during the last business cycle of 2017-2020, the average number of unfilled manufacturing jobs was 430,000. During only two months of that cycle did unfilled openings barely reach 500,000.

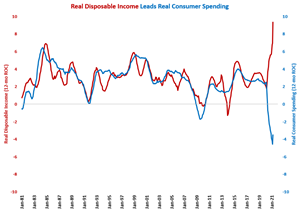

Unlike most other economic data points being reported right now, changes in real disposable income are not being affected by easy comparisons from one year ago when the economy was locked down. In fact, real disposable income in March 2020 was only 1.4% below the all-time high in disposable income. The massive increase in disposable income is purely a result of record levels of government transfer payments.

Compared with one year ago, durable goods spending increased 44.0%, which was the fastest rate of month-over-month growth ever and the only month ever with growth faster than 24%. Of course, this incredible rate of growth was partially a result of an easy comparison with March 2020 due to the start of the economic lockdown.

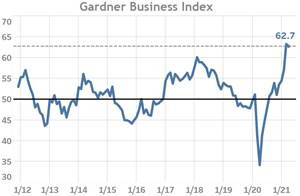

The GBI fell slightly after an 8-month trend of accelerating expansion. The latest reading was supported by readings for supplier deliveries, production and new orders but weighed down by employment and exports.

February cutting tool orders were the third highest since the economic lockdown started in March 2020. And, the GBI: Metalworking reached an all-time high in March on strength in new orders, production, and backlogs. This indicates that cutting tool orders should see strong growth in the second and third quarters of 2021.

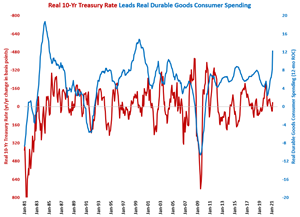

That the cost of goods and services (inflation) is rising faster than the cost of borrowing money suggests that the economy has come to an incredible rate intersection. This is particularly true in the “goods” space where inflation is at 5.4% according to the Bureau of Economic Analysis.

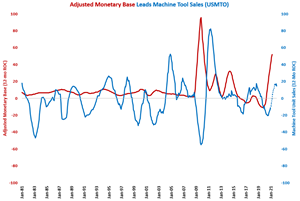

Much of the coronavirus stimulus from the government is still in place. Further, as of this writing, President Biden will announce his third $1 trillion stimulus plan since he took office at the beginning of the year. Therefore, the monetary base will likely continue to grow, which generally leads to accelerating growth in capital equipment spending.

As the threat of COVID-19 subsides, the team at Gardner Intelligence eagerly anticipates getting back on the speaking circuit. Here are some of the highlights from Michael Guckes’ presentation at the Carbon Fiber 2019 event showing what the Gardner Business Index (GBI) has to offer manufacturers looking to optimize their business success.

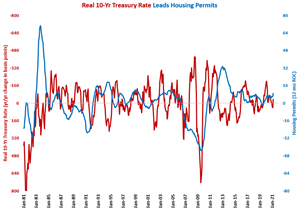

It has taken 15 years, unprecedented government stimulus, and a pandemic that drove virtually all office workers to work from home and move out of big cities for housing permits to return to levels seen prior to the housing bubble bursting in late 2006 and early 2007. This is leading to strong growth in the appliance and off-road/construction machinery industries, in particular.

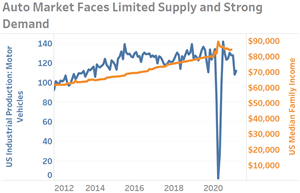

Recent months of vehicle sales have been suppressed by limited production resulting from supply chain disruptions. Despite repressed sales volumes due to limited supply, it is clear that demand for vehicles is red-hot when one examines pricing and loan data.

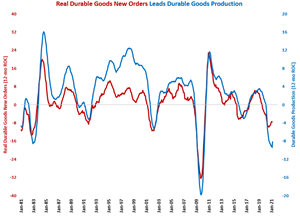

While the durable goods production index had an easy comparison in March 2021 with March 2020, the index did increase to its second-highest level since November 2019. Leading indicators such as durable goods new orders and consumer durables goods spending are pointing to faster growth in production in the months ahead.

Having surpassed the 1-year mark since COVID-19 forced the shutdown of much of the global economy, expect to see a swelling number of articles report drastic growth in virtually everything. This will require business leaders and forward-looking decision makers to take additional precautions when using new data releases over the coming months and longer.