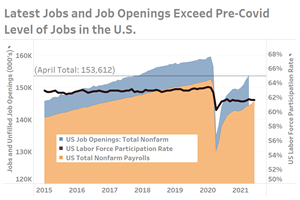

Struggling supply chains explain only part of the story behind the inability of industry to keep up with the demand for goods and services and the consequential rise in prices. As America was putting the worse of COVID behind it during the first half of 2021, a large proportion of the workforce failed to return. Just prior to the pandemic, the labor force participation rate was just over 63%. That rate then fell to 60% with the forced closure of large portions of the select industries, but then quickly rebounded to 61.7% by September 2020. In the 9 months that followed, the labor participation rate would remain virtually unchanged.

Business Activity Advances to the Second-Highest Reading in Recorded History

After moving lower during the past two months, the Gardner Business Index (GBI) rebounded to a near all-time high of 63.1.

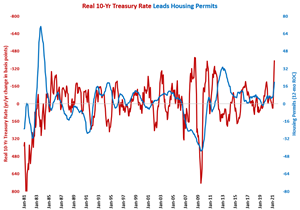

Compared with the last two months, housing permits were down about 10% in May. However, the year-over-year change in the real 10-year Treasury rate went down significantly, which is normally a positive sign for growth in housing permits.

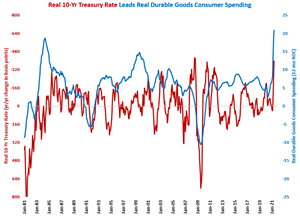

Without an easy comparison with last year due to the economic lockdown, May’s consumer durable goods spending increased more than 25% compared with one year ago.

United Airlines announced on June 29, 2021 the purchase of 270 new Boeing and Airbus aircraft. This represents the largest U.S. carrier order for new aircraft since 2011. Combined with the airline’s existing order book, the company now has in excess of 500 new narrow-body aircraft under contract. According to the company, the latest order consists of 50 737 MAX 8s, 150 737 MAX 10s and 70 A321neos.

Using some quick math and help from CompositesWorld’s editor-in-chief Jeff Sloan, the latest order would require 2.12 million pounds of composite materials. The breakout, per Gardner Intelligence’s calculations, is that just more than 850,000 pounds would be needed to fulfill the Airbus portion of the order, and 1.27 million pounds would be needed for the Boeing portion.

Beyond the benefits to the composites industry, the order is a boost to the airline industry’s confidence in the 737 MAX aircraft and the forecasted growth of the civilian aviation market throughout the 2020s and beyond.

The annual rate of change in the GBI: Metalworking grew at an accelerating rate for the third consecutive month, indicating that the annual rate of contraction in cutting tool orders has bottomed and cutting tool orders should be increasing throughout 2021.

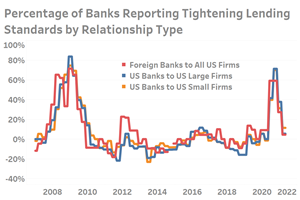

The latest available bank lending standards data from the Federal Deposit Insurance Corporation (FDIC) indicate that many types of banks have to some degree relaxed their commercial and industrial (C&I) lending standards in the U.S. in the early months of 2021. Easing standards allow for the great flow of credit which supports the business cycle and a growing economy driven by business investments.

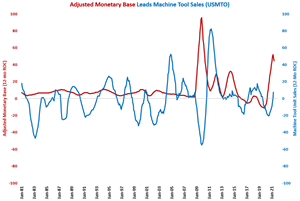

While month-over-month growth is slowing, the recent rapidly accelerating growth in the monetary base should eventually lead to rapidly accelerating growth in machine tool orders and capital equipment in general. That accelerating growth in capital equipment orders should last into 2022.

April 2021 shipments of industrial machinery reached a multi-year high according to the Bureau of Labor Statistics, up 18.6% from a year ago.

In May, durable goods capacity utilization was 74.4%. For the last five months, capacity utilization was running at a rate similar to the rate prior to the economic lockdown.

The Wall Street Journal published an article on June 22nd, 2021, titled “Wage Gains at Factories Fall Behind Growth in Fast Food” (https://www.wsj.com/articles/wage-gains-at-factories-fall-behind-growth-in-fast-food-11624354200). The article is a great reminder that manufacturing leaders can win over prospective employees through creative “win-win” plans. Such plans often involve career-training and advancement, giving away tools or other incentives for notable performance. Other incentives that manufacturers are providing which set them apart from other employers include gym memberships or even access to an on-site gym. There are also many low-cost and free incentives that have been shared with me in the past such as company-sponsored ball teams or Friday lunch grill outs in the parking lot. The example in the article of having a Spanish-speaking manufacturing line, where workers who feel more comfortable speaking Spanish can work together on a particular line is yet another “free” idea that may be a strong incentive for some prospective workers.

The key leading indicator of production – durable goods new orders – has bottomed out, according to its rate of change, and is indicating that durable goods production should see accelerating growth in the second half of 2021.