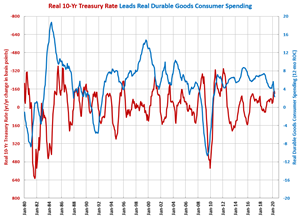

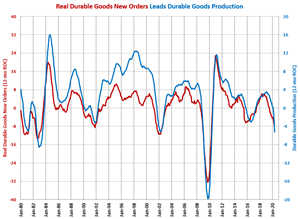

May consumer durable goods spending returned to pre-pandemic levels based on strength in appliance, electronics, motor vehicle and part, and pleasure boat spending.

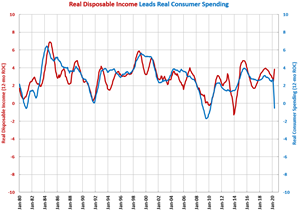

May 2020 was the second highest level of real disposable income ever. However, it was more than $800 billion lower than the income level in April

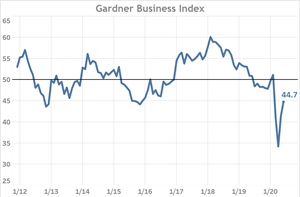

June Survey Registers Second Month of Slowing Decline in Manufacturing

In May, the annual rate of growth decelerated to 4.4%, which made it the ninth-straight month of growth but the second month of decelerating growth.

Gardner Intelligence providing free access to its 2020/2021 electronics end-market webinar hosted on June 17th, 2020.

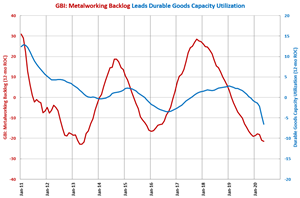

In May, durable goods capacity utilization was 57.1%, which was a modest improvement over April. Compared with one year ago, capacity utilization contracted 24.4%.

Every industry segment was contracting at a faster annual rate in May except for electronics and military. Both of these segments were growing at a slower annual rate.

To learn about the latest manufacturing trends in the electronics market?

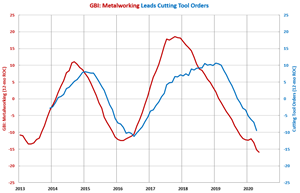

The annual rate of contraction in cutting tool orders was 9.5%, which was the fastest rate of contraction since August 2016. This contraction was as expected based on the Gardner Business Index.

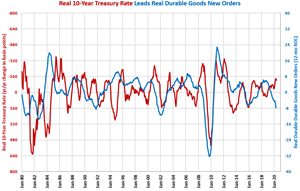

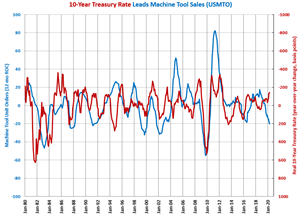

In May, the nominal 10-year Treasury rate was 0.67%, which was the third month in a row and the third month ever that the monthly average was below 1%. Also, this month’s rate was just 0.01 basis points more than last month.

While machine tool orders continue to contract at an accelerating rate, several of the early leading indicators of machine tool orders have trended in a positive direction for a number of months.

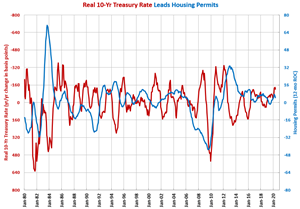

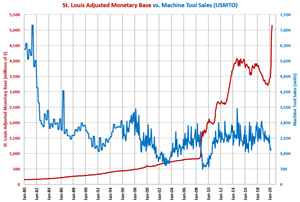

The recent rapidly accelerating growth in the monetary base should eventually lead to accelerating growth in machine tool orders and capital equipment in general. Based on the historical relationship, machine tool orders should bottom sometime between September 2020 and February 2021.