Consumer purchases of vehicles in the second half of 2020 have been surprisingly strong. In an unexpected move, luxury brands and pick-up trucks have led the rebound. All of this has been made possible by low interest rates and increased borrowing in the auto-loan market.

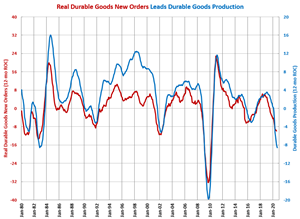

The recovery in durable goods production took a slight pause in September, but leading indicators still point to more upside in production.

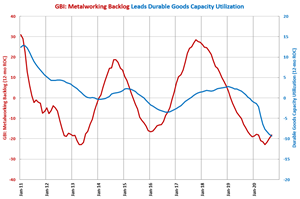

The rate of contraction in durable goods capacity utilization should bottom out in the 4th quarter of 2020, according to the Gardner Business Index.

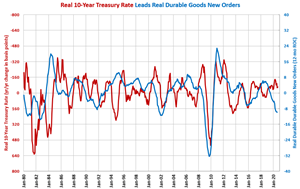

The Federal Reserve has stated it will not pursue negative interest rates. Therefore, the only way for the change to be more negative is for inflation to increase, which is why the Federal Reserve has stated a new policy of average inflation targeting.

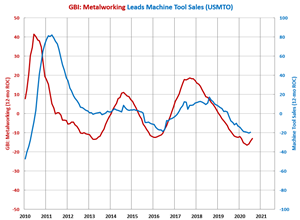

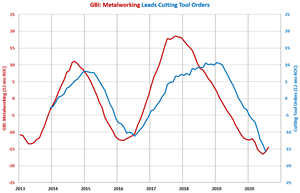

The trend in the GBI: Metalworking indicates that machine tool orders will bottom out sometime between September and the first quarter of 2021.

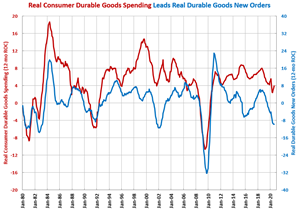

A burst in consumer durable goods spending indicates that the annual rate of contraction in durable goods new orders may be near a bottom.

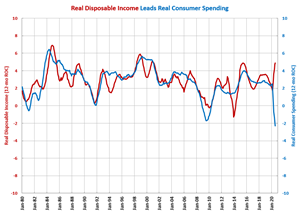

While disposable income growth was above its historic average rate, a significantly higher proportion of income was still coming from government transfer payments.

Spending patterns are changing due to the pandemic. Service and experience items are out. Goods that allow more isolated entertainment or tie in with a life of working from home are in.

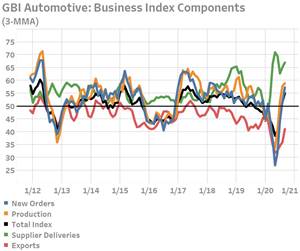

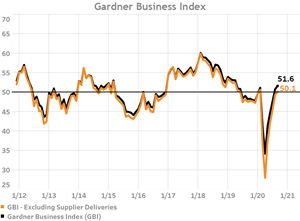

The Gardner Business Index reported a second consecutive month of expansionary activity in September. Large manufacturers and those serving the automotive and medical industries helped propel the Index higher.

A significant change in California’s regulation of the state’s automotive market has significant ramifications for both the industry and the entire automotive supply chain.

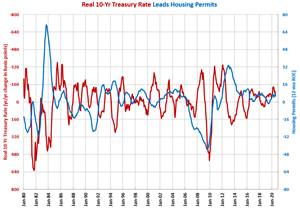

Total permits in the three-month period ending August 2020 were the highest three-month total since July 2007.

Recent changes in the Gardner Business Index indicate that the annual rate of contraction in cutting tool orders is nearing a bottom.