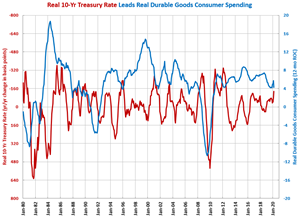

The month-over-month rate of contraction for durable goods spending was -11.2%, which was the fastest rate of contraction since April 2009.

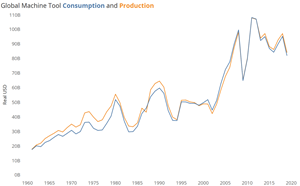

After increasing machine tool purchasing for the past two years, 12 of the top 15 machine tool consuming countries decreased in 2019 in the midst of a worldwide downturn. But in a sign of reshoring, the U.S. increased its share overall, and machine tool purchasing by Mexico increased.

According to the most recent survey conducted by Gardner Intelligence, 27% of manufacturers plan to invest in their business/facilities in the next six months with an additional 15% planning to invest after six months. Further, 90% of manufacturers say this is at least a moderate priority while 40% report it is a moderately high or very high priority.

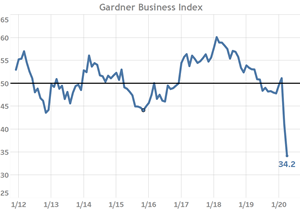

April’s reading of 34.2 signaled that overall business activity conditions continued to slow further after falling sharply in March.

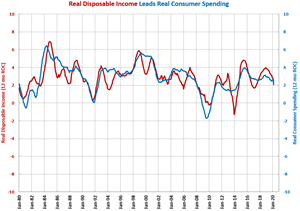

Real disposable income grew just 0.1% compared with one year ago and reached its lowest level since May 2019.

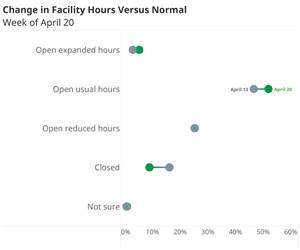

The percent of manufacturers that were closed dropped to 9% from 16% the week prior. That decrease was split between manufacturers open usual hours or expanded hours. Meanwhile, nearly 50% of manufacturers were operating with some level of reduced staff.

March housing permits were at their highest level since October 2019.

February cutting tool orders were $188.2 million, down 9.5% from one year ago.

In the most recent survey, there was a notable decrease in the percent of manufacturers serving the medical industry, 32% in the most recent week versus 41% the week prior. This seemed to have a significant impact on the results of the survey and indicated that those manufacturers not serving the medical industry were facing a different situation than those serving the medical industry.

Compared with one year ago, capacity utilization contracted 10.9%. This was the 10th month in a row and the 11th of the last 12 months that capacity utilization contracted.

Compared with one year ago, the index contracted 9.7%, which was the seventh straight month of contraction.

There is a strong relationship between the unemployment rate and the number of delinquent and defaulted loans. Since the first jump in unemployment claims on March 21st and through April 11th, over 22 million people have filed unemployment insurance claims. This vast increase in unemployment suggest that near-term credit conditions are very likely to deteriorate.